A solvency statement can be a useful tool to reduce share capital. But what is a solvency statement and why should you reduce share capital?

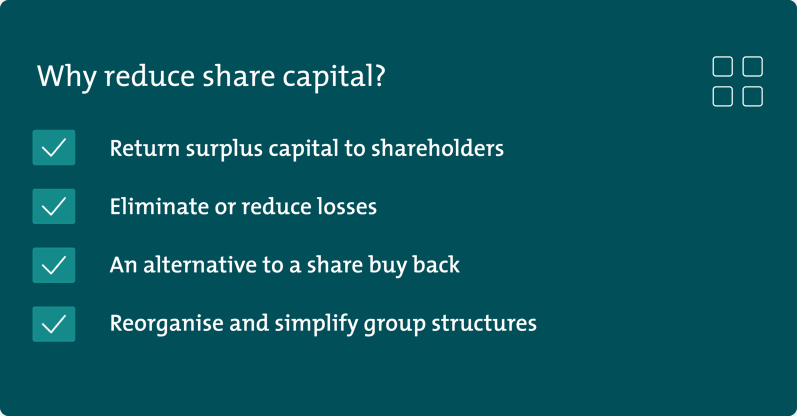

Why would a company reduce its share capital?

There are various commercial reasons for a company to reduce its share capital, such as:

- To return surplus capital to shareholders which is no longer required by the company;

- To eliminate or reduce losses of the company to allow it (for example) to declare dividends to shareholders;

- An alternative to a share buyback where the company does not have sufficient distributable reserves; or

- To reorganise and simplify group structures.

How can a company reduce its share capital?

The Companies Act 2006 prescribes two ways for a company to reduce its share capital, both of which require a resolution of at least 75% of the eligible members of the company (special resolution), which are:

- By special resolution with the confirmation of the court; and

- By special resolution supported by a solvency statement of the directors.

The solvency statement procedure is only available to private companies and the company must not be prohibited from reducing its share capital by its articles of association.

What is a solvency statement?

A solvency statement is a statement in writing signed by all directors which states that, as regards the company's situation at the date of the statement:

- There are no grounds on which the company could be found to be unable to pay or otherwise discharge its debts; and

- The company will be able to pay or discharge its debts as they fall due during the 12 months immediately following the date of the statement, or, if it is intended to commence the winding up of the company within 12 months of the date of the statement, that the company will be able to pay or discharge its debts in full within 12 months of the commencement of the winding-up.

The statement should not be made more than 15 days before the date of the passing of the shareholder’s special resolution.

Are there any sanctions on directors for providing solvency statements without having reasonable grounds for the opinions contained in them?

The Companies Act 2006 states that if the directors make a solvency statement without having reasonable grounds for the opinions expressed in it, an offence is committed by every director who is in default which can lead to imprisonment and/or a fine.

It is therefore important that directors are aware of the financial status of the company so they can make a considered decision on whether to provide the solvency statement.

What must the directors consider before they provide the statement?

- The directors should consider carefully the financial position of the company and the effect of the reduction of capital.

- They should take account of all the company’s liabilities (including prospective and contingent liabilities) of the company for at least the next 12 months.

- The Company Law Committee of the City of London Law Society has issued a memorandum highlighting practical steps that directors can take before they make a statement of solvency to reduce the risk of committing an offence under the Companies Act 2006, including:

- To consider appropriate factors and potential threats to the company's business model such as the potential insolvency of suppliers and loss of customers;

- Although it is not necessary under the Companies Act 2006, to obtain advice from independent third parties, such as accountants or auditors to help the directors reach their decision or to give them comfort that their opinions are reasonable; and

- To keep a record of the information which they have considered to show that they have exercised reasonable care, skill and diligence in forming their decisions.

- The directors should also have regard to their common law and equitable duties and their statutory duties under the Companies Act 2006, including the duties to act within their powers (section 171), to promote the success of the company (section 172) and to exercise reasonable care, skill and diligence (section 174).

When will the court procedure be appropriate?

As stated above, the solvency statement procedure is only available to private companies and therefore public companies must use the court-approved procedure in order to reduce their share capital.

The procedure may not always be the appropriate method for carrying out a reduction of capital in private companies, particularly when all of the directors are not willing to sign the solvency statement or when the directors would prefer the comfort of obtaining court approval if there is the possibility of an objection to the reduction from creditors.

The solvency statement procedure for reducing share capital introduced for private companies under the Companies Act 2006 is a simpler and more cost-effective procedure for private companies seeking to reduce share capital than the court-approved procedure.

Directors who provide solvency statements should do so only after taking into account all the company's liabilities for at least the next 12 months otherwise they run the risk of committing an offence under the Companies Act 2006.

If your company is considering carrying out a reduction of capital, or you are a director who is being asked to provide a solvency statement, and you require further advice or guidance, please contact our company law solicitors.

A version of this article was first published on 12 Oct 2017